Thermoplastic Pipe Market

Thermoplastic Pipe Market Forecasts to 2028 – Global Analysis By Polymer Type, Product Type (Reinforced Thermoplastic Pipes (RTP), Thermoplastic Composite Pipes (TCP)), Application, End User, and By Geography

|

Years Covered |

2020-2028 |

|

Estimated Year Value (2021) |

US $2.52 BN |

|

Projected Year Value (2028) |

US $3.67 BN |

|

CAGR (2021 - 2028) |

5.5% |

|

Regions Covered |

North America, Europe, Asia Pacific, South America, and Middle East & Africa |

|

Countries Covered |

US, Canada, Mexico, Germany, UK, Italy, France, Spain, Japan, China, India, Australia, New Zealand, South Korea, Rest of Asia Pacific, South America, Argentina, Brazil, Chile, Middle East & Africa, Saudi Arabia, UAE, Qatar, and South Africa |

|

Largest Market |

North America |

|

Highest Growing Market |

Asia Pacific |

According to Stratistics MRC, the Global Thermoplastic Pipe Market is accounted for $2.52 billion in 2021 and is expected to reach $3.67 billion by 2028 growing at a CAGR of 5.5% during the forecast period. Thermoplastic pipes are primarily used in the transportation of solids, liquids, and gases. They can withstand high temperatures, harsh chemicals, and long-term cyclic loading. Industries such as chemical, mining & dredging, and others widely use thermoplastic pipes. Thermoplastic pipes have unique properties such as flexibility, excellent chemical resistance, high mechanical strength, greater flow, and rust-resistant features.

Market Dynamics:

Driver:

Growing applications across offshore and onshore production activities

The oil & gas industry uses steel as a key material in manufacturing a variety of tubes and pipes. In the onshore industry, steel continues to be used dominantly in products such as coiled tubing and flow lines. In addition, thermoplastic composites are primarily used for offshore applications, such as chemical injection pipes and risers. Its properties, such as wear and corrosion resistance, better stiffness, and strength with respect to changes in temperature and deformation due to stress, make it highly effective for underwater applications. Offshore drilling and production activities are expected to increase in the next five years at a greater pace than onshore activities, given the increasing importance of deep and ultra-deepwater oil & gas production and exploration activities, as demand for fossil fuels has intensified. Therefore, thermoplastic composites’ application in offshore products, such as flowlines, umbilical, and risers, is likely to drive the thermoplastic pipe market in the oil & gas industry.

Restraint:

High cost of thermoplastic composite pipes

Thermoplastic pipes made from engineering thermoplastic grades such as polyvinyl chloride (PVC) and polyethylene (PE) have been used extensively due to their cost-effectiveness and excellent chemical resistance properties. Compared with steel, composite pipes made of PEEK or polyphenylene sulfide (PPS) cost 20–100 times more, making its application impossible for products such as pipes, thus becoming the most common obstacle for the thermoplastic pipe market. Higher grades of thermoplastics, such as polyether ether ketone (PEEK), have limited applications in seals and wirelines as they are expensive. These pipes provide good abrasion resistance, low flammability, and reduced emission of smoke and toxic gases, but they also have high raw material and fabrication costs.

Opportunity:

Increasing exploration and production activities

The temperature and pressure ratings are high in deep and ultra-deepwater and increased CO2 and H2S content scour and weaken steel. Also, in deepwaters, increased pressure and currents drag the pipes through the water. To overcome these problems, companies produce flexible pipes for the oil & gas industry by winding layers of thermoplastic composite reinforced with glass or carbon fibers around a polymer liner. As the oil & gas reserves in shallow waters are running dry, producers are turning to deep- and ultra-deepwater off the coasts of Brazil, Norway, Angola, and the US. For instance, in May 2019, Strohm collaborated with SÍMEROS TECHNOLOGIES, an engineering company, to deliver Thermoplastic Composite Pipe (TCP) risers in the deepwater region of Brazil. Bringing the fluids through 3,000 m of water to the surface poses various challenges for well operators. Moreover, thermoplastic composite pipes are much lighter than flexible steel pipes, so operators can use simpler and less expensive equipment to install them. Additionally, the ease of handling and the potential use of “no-dig” technology for installing the flexible pipes, which can be delivered to the site in long coils, help reduce jointing and traffic disruption. Therefore, the benefits of using flexible composite pipes in deep- and ultra-deepwater applications are expected to pose more opportunities for the thermoplastic pipe market.

Threat:

Problems in large-scale manufacturing

Thermoplastic composite pipes are customized products that require modifications, depending on end-use conditions, such as pressure, temperature, and corrosion. Thermoplastic composite pipe fabricators for the oil & gas industry usually have to procure raw materials (polymer) directly from the manufacturers because the fabricators have to work in sync with the operational requirements of oil companies and the quality of material provided by suppliers. Subsequently, the modifications are usually in polymer composition or processing conditions, which can be carried out only if there is close coordination between polymer manufacturers and the pipe fabricator. This constraint in standardization makes large-scale manufacturing of composite pipes a difficult prospect, contributing to the overall high cost of thermoplastic pipes.

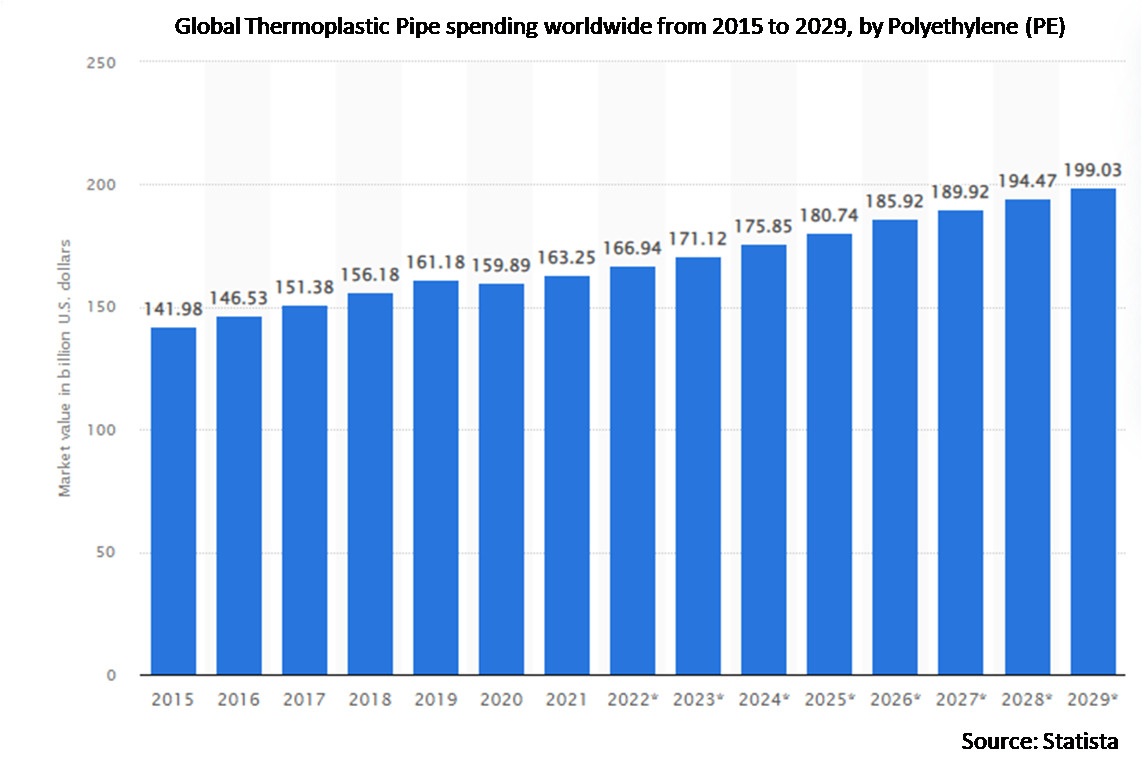

The polyethylene (PE) segment is expected to be the largest during the forecast period

The polyethylene (PE) segment is estimated to have a lucrative growth. There are two variants of PE pipes available in the market, i.e., PEX (cross-linked polyethylene) and HDPE (high-density polyethylene pipes). The crosslinked structure of polyethylene enhances the toughness and temperature resistance of the material. This enables the content to be specified for use in more harsh environments both at lower and higher temperatures. Lightweight, flexible, and easy to weld properties of polyethylene (PE) is expected to foster its inclination in the thermoplastic pipe market.

The oil & gas segment is expected to have the highest CAGR during the forecast period

The oil & gas segment is anticipated to witness the fastest CAGR growth during the forecast period. The oil & gas segment uses thermoplastic pipes for various applications, such as high-pressure water injection pipelines, water transport & distribution, effluent water disposal, temporary surface lines, good intervention, and seawater intake & discharge lines. By geography, the Asia Pacific is going to have lucrative growth due to urbanization and industrialization growth along with increasing mining activities in China and India.

Region with largest share:

North America is projected to hold the largest market share during the forecast period due to the increasing oil and gas exploration and production activities and the discovery of new oil and gas reserves. Acceptance of PP-RCT (PolyPropylene-Random Crystallinity Temperature) is driving the market in North America, which is making it easier for engineers and builders to replace traditional materials with thermoplastic piping systems.

Region with highest CAGR:

Asia Pacific is projected to have the highest CAGR over the forecast period. The growth of the Asia Pacific market is driven by urbanization and industrialization growth along with increasing mining activities in China, Australia, and India. With an increasing population in the region, the demand for water transport and energy demand is expected to increase during the forecast period. Water, an essential commodity, is mostly transported through PVC pipes, while oil & gas are mostly transported through polyethylene pipes. Asia-Pacific, despite having a lower level of urbanization, the region is home to nearly 54% of the global population. Between the period 2018 and 2050, India and China are expected to account for nearly 30% of the global projected urban population. The increase in urbanization is expected to increase the demand for oil & gas and water transportation pipeline over upcoming years.

Key players in the market:

Some of the key players profiled in the Thermoplastic Pipe Market include Advanced Drainage Systems Inc., Aetna Plastics, Airborne Oil & Gas B.V., AMIANTIT Service GmbH, Chevron Phillips Chemical Company, Future Pipe Industries, Georg Fischer Piping Systems Ltd., IPEX Inc., KWH Pipe, Master Tech Company FZC, National Oilwell Varco, Pipelife Nederland BV, Prysmian Group, Simtech, and Technip.

Key Developments:

In November 2019, IPEX completed the stock purchase of pipe producer Silver Line Plastics LLC. The deal brought together No.8 and No. 34 pipe, tubing extruders, and profile with an estimated sales value of USD 460 million and USD 140 million, respectively.

In January 2020, Advanced Drainage Systems acquired the assets of Plastic Tubing Industries (PTI), a manufacturer of HDPE pipes and related accessories. The acquisition increased the company’s customer base and capacity in Southeast US. With this step, it is expected to increase its manufacturing footprint in Georgia and Texas and add production capacity to the existing manufacturing facilities in Florida.

In October 2021, TechnipFMC acquired the outstanding shares of Magma Global; the company will use Magma Global's technology to manufacture Thermoplastic Composite Pipes (TCPs) using PEEK polymer. TechnipFMC will combine Magma Global’s expertise with its flexible pipe technology to create a Hybrid Flexible Pipe (HFP) that will be deployed in the pre-salt fields of Brazil.

Polymer Types Covered:

• Polyethylene (PE)

• Polypropylene (PP)

• Polyvinylidene Fluoride (PVDF)

• Polyvinyl Chloride (PVC)

• Other Polymer Types

Product Types Covered:

• Reinforced Thermoplastic Pipes (RTP)

• Thermoplastic Composite Pipes (TCP)

Applications Covered:

• Onshore

• Offshore

End Users Covered:

• Mining & Dredging

• Oil & Gas

• Utilities & Renewables

• Water & Wastewater

• Chemical

• Municipal

Regions Covered:

• North America

o US

o Canada

o Mexico

• Europe

o Germany

o UK

o Italy

o France

o Spain

o Rest of Europe

• Asia Pacific

o Japan

o China

o India

o Australia

o New Zealand

o South Korea

o Rest of Asia Pacific

• South America

o Argentina

o Brazil

o Chile

o Rest of South America

• Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2020, 2021, 2022, 2025, and 2028

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

• Company Profiling

o Comprehensive profiling of additional market players (up to 3)

o SWOT Analysis of key players (up to 3)

• Regional Segmentation

o Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

• Competitive Benchmarking

o Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

2.1 Abstract

2.2 Stake Holders

2.3 Research Scope

2.4 Research Methodology

2.4.1 Data Mining

2.4.2 Data Analysis

2.4.3 Data Validation

2.4.4 Research Approach

2.5 Research Sources

2.5.1 Primary Research Sources

2.5.2 Secondary Research Sources

2.5.3 Assumptions

3 Market Trend Analysis

3.1 Introduction

3.2 Drivers

3.3 Restraints

3.4 Opportunities

3.5 Threats

3.6 Product Analysis

3.7 Application Analysis

3.8 End User Analysis

3.9 Emerging Markets

3.10 Impact of Covid-19

4 Porters Five Force Analysis

4.1 Bargaining power of suppliers

4.2 Bargaining power of buyers

4.3 Threat of substitutes

4.4 Threat of new entrants

4.5 Competitive rivalry

5 Global Thermoplastic Pipe Market, By Polymer Type

5.1 Introduction

5.2 Polyethylene (PE)

5.3 Polypropylene (PP)

5.4 Polyvinylidene Fluoride (PVDF)

5.5 Polyvinyl Chloride (PVC)

5.6 Other Polymer Types

5.6.1 Polyether Ether Ketone (Peek)

5.6.2 Polyamide (PA)

5.6.3 Forced Reinforced Plastics (FRP)

5.6.4 Polytetrafluoroethylene (PTFE)

6 Global Thermoplastic Pipe Market, By Product Type

6.1 Introduction

6.2 Reinforced Thermoplastic Pipes (RTP)

6.3 Thermoplastic Composite Pipes (TCP)

7 Global Thermoplastic Pipe Market, By Application

7.1 Introduction

7.2 Onshore

7.3 Offshore

8 Global Thermoplastic Pipe Market, By End User

8.1 Introduction

8.2 Mining & Dredging

8.3 Oil & Gas

8.4 Utilities & Renewables

8.5 Water & Wastewater

8.6 Chemical

8.7 Municipal

9 Global Thermoplastic Pipe Market, By Geography

9.1 Introduction

9.2 North America

9.2.1 US

9.2.2 Canada

9.2.3 Mexico

9.3 Europe

9.3.1 Germany

9.3.2 UK

9.3.3 Italy

9.3.4 France

9.3.5 Spain

9.3.6 Rest of Europe

9.4 Asia Pacific

9.4.1 Japan

9.4.2 China

9.4.3 India

9.4.4 Australia

9.4.5 New Zealand

9.4.6 South Korea

9.4.7 Rest of Asia Pacific

9.5 South America

9.5.1 Argentina

9.5.2 Brazil

9.5.3 Chile

9.5.4 Rest of South America

9.6 Middle East & Africa

9.6.1 Saudi Arabia

9.6.2 UAE

9.6.3 Qatar

9.6.4 South Africa

9.6.5 Rest of Middle East & Africa

10 Key Developments

10.1 Agreements, Partnerships, Collaborations and Joint Ventures

10.2 Acquisitions & Mergers

10.3 New Product Launch

10.4 Expansions

10.5 Other Key Strategies

11 Company Profiling

11.1 Advanced Drainage Systems Inc.

11.2 Aetna Plastics

11.3 Airborne Oil & Gas B.V.

11.4 AMIANTIT Service GmbH

11.5 Chevron Phillips Chemical Company

11.6 Future Pipe Industries

11.7 Georg Fischer Piping Systems Ltd.

11.8 IPEX Inc.

11.9 KWH Pipe

11.10 Master Tech Company FZC

11.11 National Oilwell Varco

11.12 Pipelife Nederland BV

11.13 Prysmian Group

11.14 Simtech

11.15 Technip

List of Tables

1 Global Thermoplastic Pipe Market Outlook, By Region (2019-2028) ($MN)

2 Global Thermoplastic Pipe Market Outlook, By Polymer Type (2019-2028) ($MN)

3 Global Thermoplastic Pipe Market Outlook, By Polyethylene (PE) (2019-2028) ($MN)

4 Global Thermoplastic Pipe Market Outlook, By Polypropylene (PP) (2019-2028) ($MN)

5 Global Thermoplastic Pipe Market Outlook, By Polyvinylidene Fluoride (PVDF) (2019-2028) ($MN)

6 Global Thermoplastic Pipe Market Outlook, By Polyvinyl Chloride (PVC) (2019-2028) ($MN)

7 Global Thermoplastic Pipe Market Outlook, By Other Polymer Types (2019-2028) ($MN)

8 Global Thermoplastic Pipe Market Outlook, By Polyether Ether Ketone (Peek) (2019-2028) ($MN)

9 Global Thermoplastic Pipe Market Outlook, By Polyamide (PA) (2019-2028) ($MN)

10 Global Thermoplastic Pipe Market Outlook, By Forced Reinforced Plastics (FRP) (2019-2028) ($MN)

11 Global Thermoplastic Pipe Market Outlook, By Polytetrafluoroethylene (PTFE) (2019-2028) ($MN)

12 Global Thermoplastic Pipe Market Outlook, By Product Type (2019-2028) ($MN)

13 Global Thermoplastic Pipe Market Outlook, By Reinforced Thermoplastic Pipes (RTP) (2019-2028) ($MN)

14 Global Thermoplastic Pipe Market Outlook, By Thermoplastic Composite Pipes (TCP) (2019-2028) ($MN)

15 Global Thermoplastic Pipe Market Outlook, By Application (2019-2028) ($MN)

16 Global Thermoplastic Pipe Market Outlook, By Onshore (2019-2028) ($MN)

17 Global Thermoplastic Pipe Market Outlook, By Offshore (2019-2028) ($MN)

18 Global Thermoplastic Pipe Market Outlook, By End User (2019-2028) ($MN)

19 Global Thermoplastic Pipe Market Outlook, By Mining & Dredging (2019-2028) ($MN)

20 Global Thermoplastic Pipe Market Outlook, By Oil & Gas (2019-2028) ($MN)

21 Global Thermoplastic Pipe Market Outlook, By Utilities & Renewables (2019-2028) ($MN)

22 Global Thermoplastic Pipe Market Outlook, By Water & Wastewater (2019-2028) ($MN)

23 Global Thermoplastic Pipe Market Outlook, By Chemical (2019-2028) ($MN)

24 Global Thermoplastic Pipe Market Outlook, By Municipal (2019-2028) ($MN)

25 North America Thermoplastic Pipe Market Outlook, By Country (2019-2028) ($MN)

26 North America Thermoplastic Pipe Market Outlook, By Polymer Type (2019-2028) ($MN)

27 North America Thermoplastic Pipe Market Outlook, By Polyethylene (PE) (2019-2028) ($MN)

28 North America Thermoplastic Pipe Market Outlook, By Polypropylene (PP) (2019-2028) ($MN)

29 North America Thermoplastic Pipe Market Outlook, By Polyvinylidene Fluoride (PVDF) (2019-2028) ($MN)

30 North America Thermoplastic Pipe Market Outlook, By Polyvinyl Chloride (PVC) (2019-2028) ($MN)

31 North America Thermoplastic Pipe Market Outlook, By Other Polymer Types (2019-2028) ($MN)

32 North America Thermoplastic Pipe Market Outlook, By Polyether Ether Ketone (Peek) (2019-2028) ($MN)

33 North America Thermoplastic Pipe Market Outlook, By Polyamide (PA) (2019-2028) ($MN)

34 North America Thermoplastic Pipe Market Outlook, By Forced Reinforced Plastics (FRP) (2019-2028) ($MN)

35 North America Thermoplastic Pipe Market Outlook, By Polytetrafluoroethylene (PTFE) (2019-2028) ($MN)

36 North America Thermoplastic Pipe Market Outlook, By Product Type (2019-2028) ($MN)

37 North America Thermoplastic Pipe Market Outlook, By Reinforced Thermoplastic Pipes (RTP) (2019-2028) ($MN)

38 North America Thermoplastic Pipe Market Outlook, By Thermoplastic Composite Pipes (TCP) (2019-2028) ($MN)

39 North America Thermoplastic Pipe Market Outlook, By Application (2019-2028) ($MN)

40 North America Thermoplastic Pipe Market Outlook, By Onshore (2019-2028) ($MN)

41 North America Thermoplastic Pipe Market Outlook, By Offshore (2019-2028) ($MN)

42 North America Thermoplastic Pipe Market Outlook, By End User (2019-2028) ($MN)

43 North America Thermoplastic Pipe Market Outlook, By Mining & Dredging (2019-2028) ($MN)

44 North America Thermoplastic Pipe Market Outlook, By Oil & Gas (2019-2028) ($MN)

45 North America Thermoplastic Pipe Market Outlook, By Utilities & Renewables (2019-2028) ($MN)

46 North America Thermoplastic Pipe Market Outlook, By Water & Wastewater (2019-2028) ($MN)

47 North America Thermoplastic Pipe Market Outlook, By Chemical (2019-2028) ($MN)

48 North America Thermoplastic Pipe Market Outlook, By Municipal (2019-2028) ($MN)

49 Europe Thermoplastic Pipe Market Outlook, By Country (2019-2028) ($MN)

50 Europe Thermoplastic Pipe Market Outlook, By Polymer Type (2019-2028) ($MN)

51 Europe Thermoplastic Pipe Market Outlook, By Polyethylene (PE) (2019-2028) ($MN)

52 Europe Thermoplastic Pipe Market Outlook, By Polypropylene (PP) (2019-2028) ($MN)

53 Europe Thermoplastic Pipe Market Outlook, By Polyvinylidene Fluoride (PVDF) (2019-2028) ($MN)

54 Europe Thermoplastic Pipe Market Outlook, By Polyvinyl Chloride (PVC) (2019-2028) ($MN)

55 Europe Thermoplastic Pipe Market Outlook, By Other Polymer Types (2019-2028) ($MN)

56 Europe Thermoplastic Pipe Market Outlook, By Polyether Ether Ketone (Peek) (2019-2028) ($MN)

57 Europe Thermoplastic Pipe Market Outlook, By Polyamide (PA) (2019-2028) ($MN)

58 Europe Thermoplastic Pipe Market Outlook, By Forced Reinforced Plastics (FRP) (2019-2028) ($MN)

59 Europe Thermoplastic Pipe Market Outlook, By Polytetrafluoroethylene (PTFE) (2019-2028) ($MN)

60 Europe Thermoplastic Pipe Market Outlook, By Product Type (2019-2028) ($MN)

61 Europe Thermoplastic Pipe Market Outlook, By Reinforced Thermoplastic Pipes (RTP) (2019-2028) ($MN)

62 Europe Thermoplastic Pipe Market Outlook, By Thermoplastic Composite Pipes (TCP) (2019-2028) ($MN)

63 Europe Thermoplastic Pipe Market Outlook, By Application (2019-2028) ($MN)

64 Europe Thermoplastic Pipe Market Outlook, By Onshore (2019-2028) ($MN)

65 Europe Thermoplastic Pipe Market Outlook, By Offshore (2019-2028) ($MN)

66 Europe Thermoplastic Pipe Market Outlook, By End User (2019-2028) ($MN)

67 Europe Thermoplastic Pipe Market Outlook, By Mining & Dredging (2019-2028) ($MN)

68 Europe Thermoplastic Pipe Market Outlook, By Oil & Gas (2019-2028) ($MN)

69 Europe Thermoplastic Pipe Market Outlook, By Utilities & Renewables (2019-2028) ($MN)

70 Europe Thermoplastic Pipe Market Outlook, By Water & Wastewater (2019-2028) ($MN)

71 Europe Thermoplastic Pipe Market Outlook, By Chemical (2019-2028) ($MN)

72 Europe Thermoplastic Pipe Market Outlook, By Municipal (2019-2028) ($MN)

73 Asia Pacific Thermoplastic Pipe Market Outlook, By Country (2019-2028) ($MN)

74 Asia Pacific Thermoplastic Pipe Market Outlook, By Polymer Type (2019-2028) ($MN)

75 Asia Pacific Thermoplastic Pipe Market Outlook, By Polyethylene (PE) (2019-2028) ($MN)

76 Asia Pacific Thermoplastic Pipe Market Outlook, By Polypropylene (PP) (2019-2028) ($MN)

77 Asia Pacific Thermoplastic Pipe Market Outlook, By Polyvinylidene Fluoride (PVDF) (2019-2028) ($MN)

78 Asia Pacific Thermoplastic Pipe Market Outlook, By Polyvinyl Chloride (PVC) (2019-2028) ($MN)

79 Asia Pacific Thermoplastic Pipe Market Outlook, By Other Polymer Types (2019-2028) ($MN)

80 Asia Pacific Thermoplastic Pipe Market Outlook, By Polyether Ether Ketone (Peek) (2019-2028) ($MN)

81 Asia Pacific Thermoplastic Pipe Market Outlook, By Polyamide (PA) (2019-2028) ($MN)

82 Asia Pacific Thermoplastic Pipe Market Outlook, By Forced Reinforced Plastics (FRP) (2019-2028) ($MN)

83 Asia Pacific Thermoplastic Pipe Market Outlook, By Polytetrafluoroethylene (PTFE) (2019-2028) ($MN)

84 Asia Pacific Thermoplastic Pipe Market Outlook, By Product Type (2019-2028) ($MN)

85 Asia Pacific Thermoplastic Pipe Market Outlook, By Reinforced Thermoplastic Pipes (RTP) (2019-2028) ($MN)

86 Asia Pacific Thermoplastic Pipe Market Outlook, By Thermoplastic Composite Pipes (TCP) (2019-2028) ($MN)

87 Asia Pacific Thermoplastic Pipe Market Outlook, By Application (2019-2028) ($MN)

88 Asia Pacific Thermoplastic Pipe Market Outlook, By Onshore (2019-2028) ($MN)

89 Asia Pacific Thermoplastic Pipe Market Outlook, By Offshore (2019-2028) ($MN)

90 Asia Pacific Thermoplastic Pipe Market Outlook, By End User (2019-2028) ($MN)

91 Asia Pacific Thermoplastic Pipe Market Outlook, By Mining & Dredging (2019-2028) ($MN)

92 Asia Pacific Thermoplastic Pipe Market Outlook, By Oil & Gas (2019-2028) ($MN)

93 Asia Pacific Thermoplastic Pipe Market Outlook, By Utilities & Renewables (2019-2028) ($MN)

94 Asia Pacific Thermoplastic Pipe Market Outlook, By Water & Wastewater (2019-2028) ($MN)

95 Asia Pacific Thermoplastic Pipe Market Outlook, By Chemical (2019-2028) ($MN)

96 Asia Pacific Thermoplastic Pipe Market Outlook, By Municipal (2019-2028) ($MN)

97 South America Thermoplastic Pipe Market Outlook, By Country (2019-2028) ($MN)

98 South America Thermoplastic Pipe Market Outlook, By Polymer Type (2019-2028) ($MN)

99 South America Thermoplastic Pipe Market Outlook, By Polyethylene (PE) (2019-2028) ($MN)

100 South America Thermoplastic Pipe Market Outlook, By Polypropylene (PP) (2019-2028) ($MN)

101 South America Thermoplastic Pipe Market Outlook, By Polyvinylidene Fluoride (PVDF) (2019-2028) ($MN)

102 South America Thermoplastic Pipe Market Outlook, By Polyvinyl Chloride (PVC) (2019-2028) ($MN)

103 South America Thermoplastic Pipe Market Outlook, By Other Polymer Types (2019-2028) ($MN)

104 South America Thermoplastic Pipe Market Outlook, By Polyether Ether Ketone (Peek) (2019-2028) ($MN)

105 South America Thermoplastic Pipe Market Outlook, By Polyamide (PA) (2019-2028) ($MN)

106 South America Thermoplastic Pipe Market Outlook, By Forced Reinforced Plastics (FRP) (2019-2028) ($MN)

107 South America Thermoplastic Pipe Market Outlook, By Polytetrafluoroethylene (PTFE) (2019-2028) ($MN)

108 South America Thermoplastic Pipe Market Outlook, By Product Type (2019-2028) ($MN)

109 South America Thermoplastic Pipe Market Outlook, By Reinforced Thermoplastic Pipes (RTP) (2019-2028) ($MN)

110 South America Thermoplastic Pipe Market Outlook, By Thermoplastic Composite Pipes (TCP) (2019-2028) ($MN)

111 South America Thermoplastic Pipe Market Outlook, By Application (2019-2028) ($MN)

112 South America Thermoplastic Pipe Market Outlook, By Onshore (2019-2028) ($MN)

113 South America Thermoplastic Pipe Market Outlook, By Offshore (2019-2028) ($MN)

114 South America Thermoplastic Pipe Market Outlook, By End User (2019-2028) ($MN)

115 South America Thermoplastic Pipe Market Outlook, By Mining & Dredging (2019-2028) ($MN)

116 South America Thermoplastic Pipe Market Outlook, By Oil & Gas (2019-2028) ($MN)

117 South America Thermoplastic Pipe Market Outlook, By Utilities & Renewables (2019-2028) ($MN)

118 South America Thermoplastic Pipe Market Outlook, By Water & Wastewater (2019-2028) ($MN)

119 South America Thermoplastic Pipe Market Outlook, By Chemical (2019-2028) ($MN)

120 South America Thermoplastic Pipe Market Outlook, By Municipal (2019-2028) ($MN)

121 Middle East & Africa Thermoplastic Pipe Market Outlook, By Country (2019-2028) ($MN)

122 Middle East & Africa Thermoplastic Pipe Market Outlook, By Polymer Type (2019-2028) ($MN)

123 Middle East & Africa Thermoplastic Pipe Market Outlook, By Polyethylene (PE) (2019-2028) ($MN)

124 Middle East & Africa Thermoplastic Pipe Market Outlook, By Polypropylene (PP) (2019-2028) ($MN)

125 Middle East & Africa Thermoplastic Pipe Market Outlook, By Polyvinylidene Fluoride (PVDF) (2019-2028) ($MN)

126 Middle East & Africa Thermoplastic Pipe Market Outlook, By Polyvinyl Chloride (PVC) (2019-2028) ($MN)

127 Middle East & Africa Thermoplastic Pipe Market Outlook, By Other Polymer Types (2019-2028) ($MN)

128 Middle East & Africa Thermoplastic Pipe Market Outlook, By Polyether Ether Ketone (Peek) (2019-2028) ($MN)

129 Middle East & Africa Thermoplastic Pipe Market Outlook, By Polyamide (PA) (2019-2028) ($MN)

130 Middle East & Africa Thermoplastic Pipe Market Outlook, By Forced Reinforced Plastics (FRP) (2019-2028) ($MN)

131 Middle East & Africa Thermoplastic Pipe Market Outlook, By Polytetrafluoroethylene (PTFE) (2019-2028) ($MN)

132 Middle East & Africa Thermoplastic Pipe Market Outlook, By Product Type (2019-2028) ($MN)

133 Middle East & Africa Thermoplastic Pipe Market Outlook, By Reinforced Thermoplastic Pipes (RTP) (2019-2028) ($MN)

134 Middle East & Africa Thermoplastic Pipe Market Outlook, By Thermoplastic Composite Pipes (TCP) (2019-2028) ($MN)

135 Middle East & Africa Thermoplastic Pipe Market Outlook, By Application (2019-2028) ($MN)

136 Middle East & Africa Thermoplastic Pipe Market Outlook, By Onshore (2019-2028) ($MN)

137 Middle East & Africa Thermoplastic Pipe Market Outlook, By Offshore (2019-2028) ($MN)

138 Middle East & Africa Thermoplastic Pipe Market Outlook, By End User (2019-2028) ($MN)

139 Middle East & Africa Thermoplastic Pipe Market Outlook, By Mining & Dredging (2019-2028) ($MN)

140 Middle East & Africa Thermoplastic Pipe Market Outlook, By Oil & Gas (2019-2028) ($MN)

141 Middle East & Africa Thermoplastic Pipe Market Outlook, By Utilities & Renewables (2019-2028) ($MN)

142 Middle East & Africa Thermoplastic Pipe Market Outlook, By Water & Wastewater (2019-2028) ($MN)

143 Middle East & Africa Thermoplastic Pipe Market Outlook, By Chemical (2019-2028) ($MN)

144 Middle East & Africa Thermoplastic Pipe Market Outlook, By Municipal (2019-2028) ($MN)

List of Figures

RESEARCH METHODOLOGY

We at ‘Stratistics’ opt for an extensive research approach which involves data mining, data validation, and data analysis. The various research sources include in-house repository, secondary research, competitor’s sources, social media research, client internal data, and primary research.

Our team of analysts prefers the most reliable and authenticated data sources in order to perform the comprehensive literature search. With access to most of the authenticated data bases our team highly considers the best mix of information through various sources to obtain extensive and accurate analysis.

Each report takes an average time of a month and a team of 4 industry analysts. The time may vary depending on the scope and data availability of the desired market report. The various parameters used in the market assessment are standardized in order to enhance the data accuracy.

Data Mining

The data is collected from several authenticated, reliable, paid and unpaid sources and is filtered depending on the scope & objective of the research. Our reports repository acts as an added advantage in this procedure. Data gathering from the raw material suppliers, distributors and the manufacturers is performed on a regular basis, this helps in the comprehensive understanding of the products value chain. Apart from the above mentioned sources the data is also collected from the industry consultants to ensure the objective of the study is in the right direction.

Market trends such as technological advancements, regulatory affairs, market dynamics (Drivers, Restraints, Opportunities and Challenges) are obtained from scientific journals, market related national & international associations and organizations.

Data Analysis

From the data that is collected depending on the scope & objective of the research the data is subjected for the analysis. The critical steps that we follow for the data analysis include:

- Product Lifecycle Analysis

- Competitor analysis

- Risk analysis

- Porters Analysis

- PESTEL Analysis

- SWOT Analysis

The data engineering is performed by the core industry experts considering both the Marketing Mix Modeling and the Demand Forecasting. The marketing mix modeling makes use of multiple-regression techniques to predict the optimal mix of marketing variables. Regression factor is based on a number of variables and how they relate to an outcome such as sales or profits.

Data Validation

The data validation is performed by the exhaustive primary research from the expert interviews. This includes telephonic interviews, focus groups, face to face interviews, and questionnaires to validate our research from all aspects. The industry experts we approach come from the leading firms, involved in the supply chain ranging from the suppliers, distributors to the manufacturers and consumers so as to ensure an unbiased analysis.

We are in touch with more than 15,000 industry experts with the right mix of consultants, CEO's, presidents, vice presidents, managers, experts from both supply side and demand side, executives and so on.

The data validation involves the primary research from the industry experts belonging to:

- Leading Companies

- Suppliers & Distributors

- Manufacturers

- Consumers

- Industry/Strategic Consultants

Apart from the data validation the primary research also helps in performing the fill gap research, i.e. providing solutions for the unmet needs of the research which helps in enhancing the reports quality.

For more details about research methodology, kindly write to us at info@strategymrc.com

Frequently Asked Questions

In case of any queries regarding this report, you can contact the customer service by filing the “Inquiry Before Buy” form available on the right hand side. You may also contact us through email: info@strategymrc.com or phone: +1-301-202-5929

Yes, the samples are available for all the published reports. You can request them by filling the “Request Sample” option available in this page.

Yes, you can request a sample with your specific requirements. All the customized samples will be provided as per the requirement with the real data masked.

All our reports are available in Digital PDF format. In case if you require them in any other formats, such as PPT, Excel etc you can submit a request through “Inquiry Before Buy” form available on the right hand side. You may also contact us through email: info@strategymrc.com or phone: +1-301-202-5929

We offer a free 15% customization with every purchase. This requirement can be fulfilled for both pre and post sale. You may send your customization requirements through email at info@strategymrc.com or call us on +1-301-202-5929.

We have 3 different licensing options available in electronic format.

- Single User Licence: Allows one person, typically the buyer, to have access to the ordered product. The ordered product cannot be distributed to anyone else.

- 2-5 User Licence: Allows the ordered product to be shared among a maximum of 5 people within your organisation.

- Corporate License: Allows the product to be shared among all employees of your organisation regardless of their geographical location.

All our reports are typically be emailed to you as an attachment.

To order any available report you need to register on our website. The payment can be made either through CCAvenue or PayPal payments gateways which accept all international cards.

We extend our support to 6 months post sale. A post sale customization is also provided to cover your unmet needs in the report.

Request Customization

We provide a free 15% customization on every purchase. This requirement can be fulfilled for both pre and post sale. You may send your customization requirements through email at info@strategymrc.com or call us on +1-301-202-5929.

Note: This customization is absolutely free until it falls under the 15% bracket. If your requirement exceeds this a feasibility check will be performed. Post that, a quote will be provided along with the timelines.

WHY CHOOSE US ?

Assured Quality

Best in class reports with high standard of research integrity

24X7 Research Support

Continuous support to ensure the best customer experience.

Free Customization

Adding more values to your product of interest.

Safe & Secure Access

Providing a secured environment for all online transactions.

Trusted by 600+ Brands

Serving the most reputed brands across the world.