Carbon Capture Utilization Market

Carbon Capture, Utilization & Storage Market Forecasts to 2028 – Global Analysis By Service (Capture, Transportation, Storage, Utilization), Technology (Pre-Combustion Capture, Post-Combustion Capture) and By Geography

|

Years Covered |

2020-2028 |

|

Estimated Year Value (2021) |

US $1.74 BN |

|

Projected Year Value (2028) |

US $7.84 BN |

|

CAGR (2021 - 2028) |

24.0% |

|

Regions Covered |

North America, Europe, Asia Pacific, South America, and Middle East & Africa |

|

Countries Covered |

US, Canada, Mexico, Germany, UK, Italy, France, Spain, Japan, China, India, Australia, New Zealand, South Korea, Rest of Asia Pacific, South America, Argentina, Brazil, Chile, Middle East & Africa, Saudi Arabia, UAE, Qatar, and South Africa |

|

Largest Market |

Asia Pacific |

|

Highest Growing Market |

Europe |

According to Stratistics MRC, the Global Carbon Capture, Utilization & Storage Market is accounted for $2.10 billion in 2021 and is expected to reach $11.69 billion by 2028 growing at a CAGR of 27.8% during the forecast period. Carbon capture, utilization, and storage is the process of capturing carbon dioxide from fuel combustion or industrial processes, the transport of this CO2 through ship or pipeline, and either its use as a resource to create valuable products or services or its permanent storage deep underground in geological formations. CCUS technologies also provide the foundation for carbon removal or negative emissions when the CO2 comes from bio-based processes or directly from the atmosphere.

Market Dynamics:

Driver:

Increasing focus on reducing CO2 emissions

The use of fossil fuels and natural gas to produce electricity is the major source of CO2 emissions worldwide. Carbon capture, utilization, and storage can prevent greenhouse gases from entering the atmosphere. Therefore, growing concerns about climate change are responsible for the increasing carbon capture, utilization, and storage adoption to reduce emissions. To support the adoption of carbon capture, utilization, and storage, governments of various countries are offering numerous advantages to achieve net-zero emissions. Some of the advantages offered by government entities are tax credit and government subsidies benefitting the plant owners.

Restraint:

Large initial investments

The cost of carbon capture and storage, including all the initial expenses and ongoing operational & maintenance expenditures of carbon capture and storage plant, is higher than non-carbon capture and storage using the same fuel and net electricity output. The efficiency penalties caused by energy absorbed in capture processes and the addition of capture-specific equipment are the major cost drivers of the CO2 capture process. Factors such as initial exploration, site assessment, and site preparation are considered to calculate storage costs. Also, there are monitoring costs, which hinder the plant manufacturers from implementing carbon capture, utilization, and storage.

Opportunity:

Growing demand for carbondioxide

Carbondioxide (CO2) is widely used in various industries, such as food & beverage, manufacturing, and metal fabrication. Earlier, most of the CO2 used for EOR techniques was recovered from naturally occurring reservoirs. However, new technologies are being developed to produce CO2 from industrial applications, such as ethanol, fertilizer, hydrogen plants, and natural gas processing, where naturally occurring reservoirs are unavailable. EOR techniques include thermal recovery, gas injection, and chemical injection. The use of CO2-EOR techniques helps produce 30–60% or more oil from reservoirs, restore reservoir pressure, reduce viscosity, decrease oil density, and increase the permeability of carbonate formations.

Threat:

Decreasing crude oil prices

Carbon dioxide is widely used for crude oil extraction. Decreasing crude oil prices are expected to be a major threat for the carbon capture, utilization, and storage market growth during the forecast period.

The energy sector segment is expected to be the largest during the forecast period

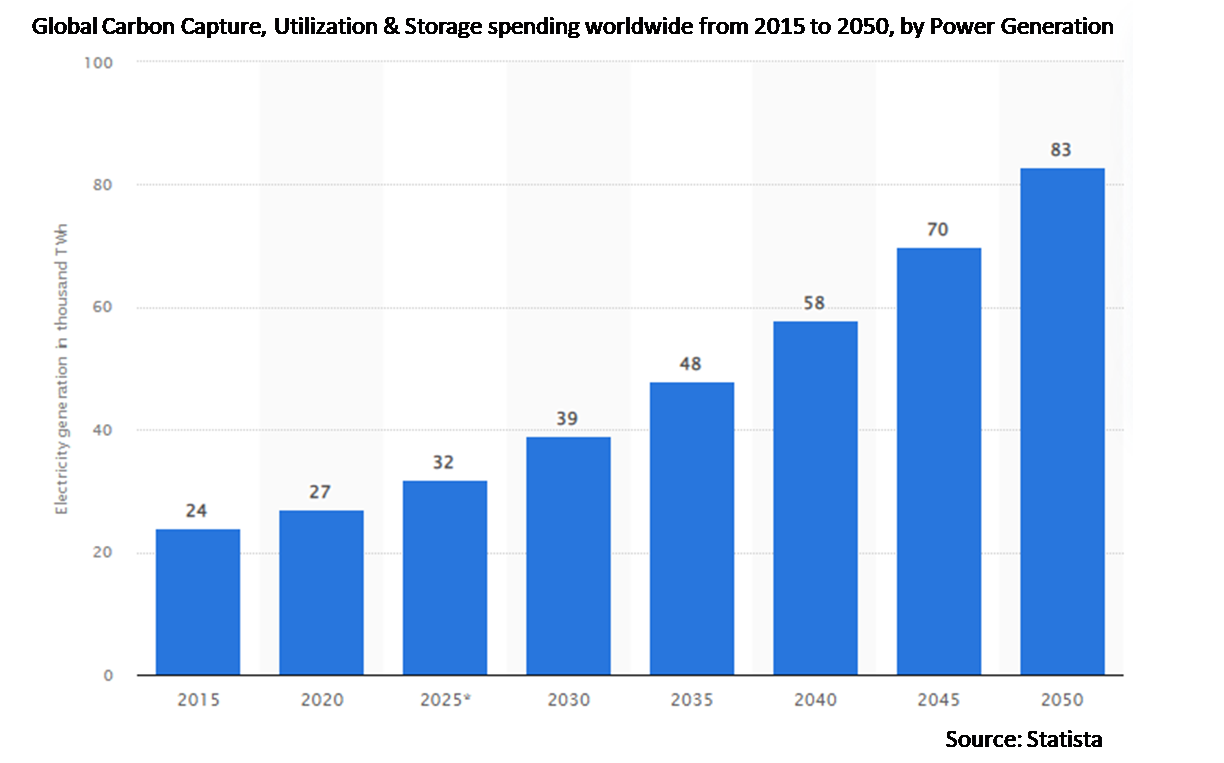

Energy sector is the fastest growing industry for carbon capture, utilization, and storage adoption. The industry generates a massive amount of CO2 and hence attracts multiple stakeholders to reduce these emissions. Fossil fuel power plants generate significant amounts of CO2 emissions into the atmosphere, which are the main cause of climate change. Among CO2 mitigation options, carbon capture and storage is considered the only technology that can significantly reduce the emissions of CO2 from fossil fuel combustion sources.

The transportation segment is expected to have the highest CAGR during the forecast period

Transportation involves carrying carbon from capture location to storage area; trucks, ships, and pipelines are the most common modes for this purpose. Pipelines are most preferred as they offer lower costs in the long run. Pipelines also have the least emission in transporting carbon, making it most effective for the cause. For commercial applications, onshore trucks are preferred, while for EOR and storage applications, pipelines are preferred both on and offshore. Pipelines are widely used for the transportation of CO2.

Region with largest share:

North America is projected to hold the largest market share owing to the rising demand from end-use industries in the region. The markets in the regions are expected to register high growth in comparison to other regions owing to the large scale development projects of carbon capture, utilization, and storage. The availability of multiple large-scale CCUS facilities in the U.S. and Canada is also a factor for the regional market growth.

Region with highest CAGR:

Europe is projected to have the highest CAGR due to the rise in number of CCUS projects in Netherlands and the U.K. Increasing applications of CCU in the enhanced oil recovery (EOR) in the oil and gas segment are expected to contribute to the growth of the market. Further, the food and beverages, chemicals, and cement industries are anticipated to be the major application segments that are expected to contribute to the growth of the European market over the forecast period.

Key players in the market

Some of the key players profiled in the Carbon Capture, Utilization & Storage Market include Mitsubishi Heavy Industries Ltd, General Electric, Siemens AG, BASF SE, Schlumberger Limited, Halliburton, ExxonMobil Corporation, Honeywell International Inc, Linde AG, Carbon Cycle Ltd, Joule Unlimited Inc, MBD Energy Ltd, Fluor Corporation, Integrated Carbon, Sequestration Pty. Ltd, Skyonic Corp, AkerSolutions, and Dioxide Materials Inc.

Key developments:

In October 2021: ExxonMobil Corporation signed an expression of interest to capture, transport and store CO2 from its Fife Ethylene Plant. It increased its participation in the Acorn carbon capture project in Scotland to achieve this.

In September 2020: Mitsubishi Shipbuilding Co., Ltd., a part of Mitsubishi Heavy Industries, Ltd. (MHI), worked with Nippon Kaiji Kyokai (Japan) and Kawasaki Kisen Kaisha, Ltd. (Japan) to conduct test operations and measurements for a small-scale ship-based CO2 capture demonstration plant. This technology is being tested to verify the equipment’s use as a marine-based CO2 capture system.

Sources Covered:

• Industrial Processes

• Power Generation

Services Covered:

• Capture

• Transportation

• Storage

• Utilization

Technologies Covered:

• Oxy-Fuel Combustion Capture

• Pre-Combustion Capture

• Post-Combustion Capture

• Industrial Separation Capture

• Inherent Separation

Applications Covered:

• Secondary Construction Materials

• Enhanced Oil Recovery (EOR)

• Without Conversion Co2 Reuse

• Feedstock for Chemicals and Polymers

End Users Covered:

• Energy Sector

• Iron & Steel

• Chemical & Petrochemical

• Oil & Gas

• Cement

• Coal & Biomass Power Plant

• Fertilizers

• Hydrogen

• Agriculture

• Food & Beverage

Regions Covered:

• North America

o US

o Canada

o Mexico

• Europe

o Germany

o UK

o Italy

o France

o Spain

o Rest of Europe

• Asia Pacific

o Japan

o China

o India

o Australia

o New Zealand

o South Korea

o Rest of Asia Pacific

• South America

o Argentina

o Brazil

o Chile

o Rest of South America

• Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2020, 2021, 2022, 2025, and 2028

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

• Company Profiling

o Comprehensive profiling of additional market players (up to 3)

o SWOT Analysis of key players (up to 3)

• Regional Segmentation

o Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

• Competitive Benchmarking

o Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

2.1 Abstract

2.2 Stake Holders

2.3 Research Scope

2.4 Research Methodology

2.4.1 Data Mining

2.4.2 Data Analysis

2.4.3 Data Validation

2.4.4 Research Approach

2.5 Research Sources

2.5.1 Primary Research Sources

2.5.2 Secondary Research Sources

2.5.3 Assumptions

3 Market Trend Analysis

3.1 Introduction

3.2 Drivers

3.3 Restraints

3.4 Opportunities

3.5 Threats

3.6 Technology Analysis

3.7 Application Analysis

3.8 End User Analysis

3.9 Emerging Markets

3.10 Impact of Covid-19

4 Porters Five Force Analysis

4.1 Bargaining power of suppliers

4.2 Bargaining power of buyers

4.3 Threat of substitutes

4.4 Threat of new entrants

4.5 Competitive rivalry

5 Global Carbon Capture, Utilization & Storage Market, By Source

5.1 Introduction

5.2 Industrial Processes

5.3 Power Generation

6 Global Carbon Capture, Utilization & Storage Market, By Service

6.1 Introduction

6.2 Capture

6.3 Transportation

6.4 Storage

6.4.1 Deep Ocean Storage

6.4.2 Geological Storage

6.4.2.1 Unmineable Coal Beds

6.4.2.2 Oil & Gas Reservoirs

6.4.2.3 Saline Aquifers

6.5 Utilization

7 Global Carbon Capture, Utilization & Storage Market, By Technology

7.1 Introduction

7.2 Oxy-Fuel Combustion Capture

7.3 Pre-Combustion Capture

7.4 Post-Combustion Capture

7.5 Industrial Separation Capture

7.6 Inherent Separation

8 Global Carbon Capture, Utilization & Storage Market, By Application

8.1 Introduction

8.2 Secondary Construction Materials

8.3 Enhanced Oil Recovery (EOR)

8.4 Without Conversion Co2 Reuse

8.5 Feedstock for Chemicals and Polymers

9 Global Carbon Capture, Utilization & Storage Market, By End User

9.1 Introduction

9.2 Energy Sector

9.3 Iron & Steel

9.4 Chemical & Petrochemical

9.5 Oil & Gas

9.6 Cement

9.7 Coal & Biomass Power Plant

9.8 Fertilizers

9.9 Hydrogen

9.10 Agriculture

9.11 Food & Beverage

10 Global Carbon Capture, Utilization & Storage Market, By Geography

10.1 Introduction

10.2 North America

10.2.1 US

10.2.2 Canada

10.2.3 Mexico

10.3 Europe

10.3.1 Germany

10.3.2 UK

10.3.3 Italy

10.3.4 France

10.3.5 Spain

10.3.6 Rest of Europe

10.4 Asia Pacific

10.4.1 Japan

10.4.2 China

10.4.3 India

10.4.4 Australia

10.4.5 New Zealand

10.4.6 South Korea

10.4.7 Rest of Asia Pacific

10.5 South America

10.5.1 Argentina

10.5.2 Brazil

10.5.3 Chile

10.5.4 Rest of South America

10.6 Middle East & Africa

10.6.1 Saudi Arabia

10.6.2 UAE

10.6.3 Qatar

10.6.4 South Africa

10.6.5 Rest of Middle East & Africa

11 Key Developments

11.1 Agreements, Partnerships, Collaborations and Joint Ventures

11.2 Acquisitions & Mergers

11.3 New Product Launch

11.4 Expansions

11.5 Other Key Strategies

12 Company Profiling

12.1 Mitsubishi Heavy Industries Ltd

12.2 General Electric

12.3 Siemens AG

12.4 BASF SE

12.5 Schlumberger Limited

12.6 Halliburton

12.7 ExxonMobil Corporation

12.8 Honeywell International Inc

12.9 Linde AG

12.10 Carbon Cycle Ltd

12.11 Joule Unlimited Inc

12.12 MBD Energy Ltd

12.13 Fluor Corporation

12.14 Integrated Carbon Sequestration Pty. Ltd

12.15 Skyonic Corp

12.16 AkerSolutions

12.17 Dioxide Materials Inc

List of Tables

1 Global Carbon Capture, Utilization & Storage Market Outlook, By Region (2020-2028) ($MN)

2 Global Carbon Capture, Utilization & Storage Market Outlook, By Source (2020-2028) ($MN)

3 Global Carbon Capture, Utilization & Storage Market Outlook, By Industrial Processes (2020-2028) ($MN)

4 Global Carbon Capture, Utilization & Storage Market Outlook, By Power Generation (2020-2028) ($MN)

5 Global Carbon Capture, Utilization & Storage Market Outlook, By Service (2020-2028) ($MN)

6 Global Carbon Capture, Utilization & Storage Market Outlook, By Capture (2020-2028) ($MN)

7 Global Carbon Capture, Utilization & Storage Market Outlook, By Transportation (2020-2028) ($MN)

8 Global Carbon Capture, Utilization & Storage Market Outlook, By Storage (2020-2028) ($MN)

9 Global Carbon Capture, Utilization & Storage Market Outlook, By Deep Ocean Storage (2020-2028) ($MN)

10 Global Carbon Capture, Utilization & Storage Market Outlook, By Geological Storage (2020-2028) ($MN)

11 Global Carbon Capture, Utilization & Storage Market Outlook, By Utilization (2020-2028) ($MN)

12 Global Carbon Capture, Utilization & Storage Market Outlook, By Technology (2020-2028) ($MN)

13 Global Carbon Capture, Utilization & Storage Market Outlook, By Oxy-Fuel Combustion Capture (2020-2028) ($MN)

14 Global Carbon Capture, Utilization & Storage Market Outlook, By Pre-Combustion Capture (2020-2028) ($MN)

15 Global Carbon Capture, Utilization & Storage Market Outlook, By Post-Combustion Capture (2020-2028) ($MN)

16 Global Carbon Capture, Utilization & Storage Market Outlook, By Industrial Separation Capture (2020-2028) ($MN)

17 Global Carbon Capture, Utilization & Storage Market Outlook, By Inherent Separation (2020-2028) ($MN)

18 Global Carbon Capture, Utilization & Storage Market Outlook, By Application (2020-2028) ($MN)

19 Global Carbon Capture, Utilization & Storage Market Outlook, By Secondary Construction Materials (2020-2028) ($MN)

20 Global Carbon Capture, Utilization & Storage Market Outlook, By Enhanced Oil Recovery (EOR) (2020-2028) ($MN)

21 Global Carbon Capture, Utilization & Storage Market Outlook, By Without Conversion Co2 Reuse (2020-2028) ($MN)

22 Global Carbon Capture, Utilization & Storage Market Outlook, By Feedstock for Chemicals and Polymers (2020-2028) ($MN)

23 Global Carbon Capture, Utilization & Storage Market Outlook, By End User (2020-2028) ($MN)

24 Global Carbon Capture, Utilization & Storage Market Outlook, By Energy Sector (2020-2028) ($MN)

25 Global Carbon Capture, Utilization & Storage Market Outlook, By Iron & Steel (2020-2028) ($MN)

26 Global Carbon Capture, Utilization & Storage Market Outlook, By Chemical & Petrochemical (2020-2028) ($MN)

27 Global Carbon Capture, Utilization & Storage Market Outlook, By Oil & Gas (2020-2028) ($MN)

28 Global Carbon Capture, Utilization & Storage Market Outlook, By Cement (2020-2028) ($MN)

29 Global Carbon Capture, Utilization & Storage Market Outlook, By Coal & Biomass Power Plant (2020-2028) ($MN)

30 Global Carbon Capture, Utilization & Storage Market Outlook, By Fertilizers (2020-2028) ($MN)

31 Global Carbon Capture, Utilization & Storage Market Outlook, By Hydrogen (2020-2028) ($MN)

32 Global Carbon Capture, Utilization & Storage Market Outlook, By Agriculture (2020-2028) ($MN)

33 Global Carbon Capture, Utilization & Storage Market Outlook, By Food & Beverage (2020-2028) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

List of Figures

RESEARCH METHODOLOGY

We at ‘Stratistics’ opt for an extensive research approach which involves data mining, data validation, and data analysis. The various research sources include in-house repository, secondary research, competitor’s sources, social media research, client internal data, and primary research.

Our team of analysts prefers the most reliable and authenticated data sources in order to perform the comprehensive literature search. With access to most of the authenticated data bases our team highly considers the best mix of information through various sources to obtain extensive and accurate analysis.

Each report takes an average time of a month and a team of 4 industry analysts. The time may vary depending on the scope and data availability of the desired market report. The various parameters used in the market assessment are standardized in order to enhance the data accuracy.

Data Mining

The data is collected from several authenticated, reliable, paid and unpaid sources and is filtered depending on the scope & objective of the research. Our reports repository acts as an added advantage in this procedure. Data gathering from the raw material suppliers, distributors and the manufacturers is performed on a regular basis, this helps in the comprehensive understanding of the products value chain. Apart from the above mentioned sources the data is also collected from the industry consultants to ensure the objective of the study is in the right direction.

Market trends such as technological advancements, regulatory affairs, market dynamics (Drivers, Restraints, Opportunities and Challenges) are obtained from scientific journals, market related national & international associations and organizations.

Data Analysis

From the data that is collected depending on the scope & objective of the research the data is subjected for the analysis. The critical steps that we follow for the data analysis include:

- Product Lifecycle Analysis

- Competitor analysis

- Risk analysis

- Porters Analysis

- PESTEL Analysis

- SWOT Analysis

The data engineering is performed by the core industry experts considering both the Marketing Mix Modeling and the Demand Forecasting. The marketing mix modeling makes use of multiple-regression techniques to predict the optimal mix of marketing variables. Regression factor is based on a number of variables and how they relate to an outcome such as sales or profits.

Data Validation

The data validation is performed by the exhaustive primary research from the expert interviews. This includes telephonic interviews, focus groups, face to face interviews, and questionnaires to validate our research from all aspects. The industry experts we approach come from the leading firms, involved in the supply chain ranging from the suppliers, distributors to the manufacturers and consumers so as to ensure an unbiased analysis.

We are in touch with more than 15,000 industry experts with the right mix of consultants, CEO's, presidents, vice presidents, managers, experts from both supply side and demand side, executives and so on.

The data validation involves the primary research from the industry experts belonging to:

- Leading Companies

- Suppliers & Distributors

- Manufacturers

- Consumers

- Industry/Strategic Consultants

Apart from the data validation the primary research also helps in performing the fill gap research, i.e. providing solutions for the unmet needs of the research which helps in enhancing the reports quality.

For more details about research methodology, kindly write to us at info@strategymrc.com

Frequently Asked Questions

In case of any queries regarding this report, you can contact the customer service by filing the “Inquiry Before Buy” form available on the right hand side. You may also contact us through email: info@strategymrc.com or phone: +1-301-202-5929

Yes, the samples are available for all the published reports. You can request them by filling the “Request Sample” option available in this page.

Yes, you can request a sample with your specific requirements. All the customized samples will be provided as per the requirement with the real data masked.

All our reports are available in Digital PDF format. In case if you require them in any other formats, such as PPT, Excel etc you can submit a request through “Inquiry Before Buy” form available on the right hand side. You may also contact us through email: info@strategymrc.com or phone: +1-301-202-5929

We offer a free 15% customization with every purchase. This requirement can be fulfilled for both pre and post sale. You may send your customization requirements through email at info@strategymrc.com or call us on +1-301-202-5929.

We have 3 different licensing options available in electronic format.

- Single User Licence: Allows one person, typically the buyer, to have access to the ordered product. The ordered product cannot be distributed to anyone else.

- 2-5 User Licence: Allows the ordered product to be shared among a maximum of 5 people within your organisation.

- Corporate License: Allows the product to be shared among all employees of your organisation regardless of their geographical location.

All our reports are typically be emailed to you as an attachment.

To order any available report you need to register on our website. The payment can be made either through CCAvenue or PayPal payments gateways which accept all international cards.

We extend our support to 6 months post sale. A post sale customization is also provided to cover your unmet needs in the report.

Request Customization

We provide a free 15% customization on every purchase. This requirement can be fulfilled for both pre and post sale. You may send your customization requirements through email at info@strategymrc.com or call us on +1-301-202-5929.

Note: This customization is absolutely free until it falls under the 15% bracket. If your requirement exceeds this a feasibility check will be performed. Post that, a quote will be provided along with the timelines.

WHY CHOOSE US ?

Assured Quality

Best in class reports with high standard of research integrity

24X7 Research Support

Continuous support to ensure the best customer experience.

Free Customization

Adding more values to your product of interest.

Safe & Secure Access

Providing a secured environment for all online transactions.

Trusted by 600+ Brands

Serving the most reputed brands across the world.