Flexible Plastic Packaging Coating Market

Flexible Plastic Packaging Coating Market Forecasts to 2032 - Global Analysis By Coating Type (Epoxy Coatings, Acrylic Coatings, Urethane & Polyurethane Coatings, Lacquer Coatings, Plasma Coatings, Polyester Coatings, Phenolic Coatings, Water-Based Coatings, Solvent-Based Coatings, UV-Curable Coatings and Other Coating Types), Material Type, Application, End User and By Geography

|

Years Covered |

2024-2032 |

|

Estimated Year Value (2025) |

US $5.10 BN |

|

Projected Year Value (2032) |

US $8.08 BN |

|

CAGR (2025 - 2032) |

6.8% |

|

Regions Covered |

North America, Europe, Asia Pacific, South America, and Middle East & Africa |

|

Countries Covered |

US, Canada, Mexico, Germany, UK, Italy, France, Spain, Japan, China, India, Australia, New Zealand, South Korea, Rest of Asia Pacific, South America, Argentina, Brazil, Chile, Middle East & Africa, Saudi Arabia, UAE, Qatar, and South Africa |

|

Largest Market |

Asia Pacific |

|

Highest Growing Market |

Middle East & Africa |

According to Stratistics MRC, the Global Flexible Plastic Packaging Coating Market is accounted for $5.10 billion in 2025 and is expected to reach $8.08 billion by 2032 growing at a CAGR of 6.8% during the forecast period. The process of applying specialized materials to flexible plastic substrates in order to improve their functionality, performance, and durability is known as flexible plastic packaging coating. These coatings have a number of uses, including strengthening mechanical strength, improving printability, offering heat resistance, and improving barrier qualities against light, oxygen, and moisture. Moreover, these coatings, which help prolong product shelf life and guarantee product safety, are frequently used in food, pharmaceutical, personal care, and industrial packaging. Materials that provide a balance between flexibility and protection without sacrificing the lightweight and affordable nature of flexible plastic packaging include acrylics, polyurethanes, and polyvinylidene chloride (PVDC).

According to the Flexible Packaging Association (FPA), the U.S. flexible packaging industry was estimated to be $42.9 billion in annual sales for 2022, with projections indicating growth to $44.7 billion in 2023. Additionally, flexible packaging represents 21% of the $180.3 billion U.S. packaging industry, making it the second-largest packaging segment behind corrugated paper at 22%.

Market Dynamics:

Driver:

Growing interest in processed and packaged foods

Convenient, readily consumable, and long-lasting food items are becoming more and more popular among consumers as a result of the global trend toward urban lifestyles and dual-income households. Because they offer superior barrier qualities, flexible plastic packaging coatings are essential for maintaining the safety, flavor, and freshness of these foods. Coatings aid in preventing food quality degradation from oxygen, moisture, and UV light. Additionally, the rapid increase in processed food consumption in developing economies, particularly in Asia-Pacific and Latin America, is driving up demand for coated flexible packaging.

Restraint:

Environmental issues and laws regarding plastic waste

Due to their role in persistent environmental pollution, governments and environmental organizations worldwide are increasingly focusing on single-use plastics, including flexible packaging. Many flexible plastic films with coatings are challenging to recycle, particularly multi-layered structures with mixed material compositions, despite their low weight and low material consumption. By adding chemical additives that are difficult to separate, coatings can make recycling even more difficult. Global plastic bags and extended producer responsibility (EPR) regulations are forcing businesses to rethink or cut back on the use of coated flexible plastics, which is slowing market growth in some areas.

Opportunity:

Growth in the need for recyclable and sustainable coatings

The creation of environmentally friendly coatings that complement the circular economy is one of the most exciting prospects. Governments, businesses, and consumers are all pushing for more environmentally friendly packaging options. Water-based, compostable, or bio-based coatings that can be applied to recyclable mono-material films are now in high demand as a result. Businesses that make such investments stand to gain access to a premium market segment as well as advantageous government incentives and regulatory frameworks that promote green packaging technologies. Furthermore, this opportunity is further strengthened by the development of easily separable multi-layer systems and de-inkable coatings.

Threat:

Technical difficulties in reusing coated materials

Multi-material laminates that are challenging to process with conventional recycling infrastructure are frequently found in coated flexible packaging structures. When coatings are chemically bonded to the substrate or heat-resistant, they can obstruct the recovery of polymers, ink, or materials. Due to this technical difficulty, the amount of post-consumer recycled (PCR) material that can be obtained from such packaging is limited, and its attractiveness is diminished in areas with inadequate recycling infrastructure. Moreover, coated flexible packaging's difficulty in recycling could become a significant competitive disadvantage as recyclability becomes a crucial criterion for both purchasing and regulations.

Covid-19 Impact:

The market for flexible plastic packaging coating was affected by the COVID-19 pandemic in a variety of ways. On the one hand, the use of coated flexible packaging increased as demand rose in critical industries like food, pharmaceuticals, and personal care, where hygienic practices, barrier protection, and longer shelf life became critical. This trend was further accelerated by the growth of home deliveries and e-commerce. However, the industry also had to deal with issues like labor shortages, supply chain disruptions, and shortages of raw materials, which made it difficult to meet delivery and production deadlines. Furthermore, the overall growth was somewhat offset by a brief decline in demand from non-essential industries like luxury goods and cosmetics.

The water-based coatings segment is expected to be the largest during the forecast period

The water-based coatings segment is expected to account for the largest market share during the forecast period. Due to their low or zero volatile organic compound (VOC) emissions, which are in line with worldwide sustainability trends, these coatings are favored for use in food, pharmaceutical, and personal care packaging. Water-based coatings are perfect for flexible substrates like polyethylene and polypropylene films because they have outstanding adhesion, printability, and barrier qualities. Their continued dominance in the market across developed and emerging regions is being driven by their growing adoption, which is bolstered by government regulations that favor eco-friendly solutions and rising demand from major FMCG brands that prioritize sustainable packaging.

The barrier coatings segment is expected to have the highest CAGR during the forecast period

Over the forecast period, the barrier coatings segment is predicted to witness the highest growth rate. because packaging that maintains content integrity and prolongs product shelf life is becoming more and more in demand. For food, beverage, pharmaceutical, and medical applications, these coatings are essential because they greatly increase resistance to moisture, oxygen, grease, and other external contaminants. Barrier coatings are becoming more and more popular as a result of the need to reduce food waste, improve product protection during transportation, and adhere to strict packaging regulations. This market is positioned as a major force behind sustainable packaging solutions of the future owing to advancements in recyclable and bio-based barrier coatings.

Region with largest share:

During the forecast period, the Asia Pacific region is expected to hold the largest market share, fueled by growing packaging industries, quick industrialization, and increased consumer demand in nations like China, India, and Japan. The demand for sophisticated flexible packaging solutions with improved barrier and protective coatings is further driven by the expansion of the food and beverage, pharmaceutical, and e-commerce industries. The region's dominance is also influenced by growing investments in technological advancements and manufacturing infrastructure. Moreover, Asia-Pacific is now the world's leading region for flexible plastic packaging coating due to its affordable production capabilities and expanding urban population, which are driving market expansion.

Region with highest CAGR:

Over the forecast period, the Middle East & Africa region is anticipated to exhibit the highest CAGR. The expansion of the retail and e-commerce industries in nations like the United Arab Emirates, Saudi Arabia, and South Africa, as well as the growing demand for packaged foods and medications, are the main drivers of this growth. Demand for cutting-edge coating technologies is also being driven by increased consumer awareness of product safety and longer shelf life. Additionally, MEA is a promising emerging market for flexible plastic packaging coatings because of investments in infrastructure development and the adoption of creative packaging solutions, which accelerate market growth in the region.

Key players in the market

Some of the key players in Flexible Plastic Packaging Coating Market include BASF SE, Kansai Paint Co., Ltd., Akzo Nobel N.V., Koninklijke DSM N.V., Bostik SA, Michelman, Inc., Jamestown Coating Technologies Company, Paramelt B.V., American Packaging Corporation, Sierra Coating Technologies LLC, Allnex Group, PPG Industries, Inc., Schmid Rhyner AG, Wacker Chemie AG and Plasmatreat GmbH.

Key Developments:

In February 2025, Akzo Nobel India has finalised a deal to sell its powder coatings business and International Research Centre (R&D) to its parent company, AkzoNobel N.V., for Rs 20.73 billion and Rs 700 million, respectively. The agreement also includes the transfer of intellectual property rights related to the decorative paints business in India, Bangladesh, Bhutan, and Nepal for Rs 11.52 billion.

In December 2024, BASF announced that it has signed a binding agreement to sell its Food & Health Performance Ingredients business to Louis Dreyfus Co. (LDC), a leading global merchant and processor of agricultural goods including high-quality, plant-based ingredients. The agreement includes a production site and state-of-the-art research and development center in Illertissen, Germany, and three application labs outside of Germany.?

In October 2024, Kansai Nerolac Paints announced that its board has approved the sale of a land parcel in Mumbai for Rs 726 crore, according to an exchange filing on the BSE. The paint maker's board has okayed its proposal to enter into an agreement with Aethon Developers Pvt. for sale of the property that is located in Mumbai's Lower Parel area.

Coating Types Covered:

• Epoxy Coatings

• Acrylic Coatings

• Urethane & Polyurethane Coatings

• Lacquer Coatings

• Plasma Coatings

• Polyester Coatings

• Phenolic Coatings

• Water-Based Coatings

• Solvent-Based Coatings

• UV-Curable Coatings

• Other Coating Types

Material Types Covered:

• Polyethylene (PE)

• Polypropylene

• Polyethylene Terephthalate (PET)

• Polyamide (PA)

• Polyvinyl Chloride (PVC)

• Polyvinylidene Chloride (PVDC)

• Ethylene Vinyl Alcohol (EVOH)

• Polystyrene (PS)

• Other Material Types

Applications Covered:

• Decorative

• Protective

• Heat Seal

• Print Primer

• Barrier Coatings

• Other Applications

End Users Covered:

• Food & Beverage Packaging

• Pharmaceutical Packaging

• Cosmetics & Personal Care Packaging

• Chemical Packaging

• Consumer Durables/Electronic Goods Packaging

• Automotive & Allied Packaging

• Other End Users

Regions Covered:

• North America

o US

o Canada

o Mexico

• Europe

o Germany

o UK

o Italy

o France

o Spain

o Rest of Europe

• Asia Pacific

o Japan

o China

o India

o Australia

o New Zealand

o South Korea

o Rest of Asia Pacific

• South America

o Argentina

o Brazil

o Chile

o Rest of South America

• Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2024, 2025, 2026, 2028, and 2032

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

• Company Profiling

o Comprehensive profiling of additional market players (up to 3)

o SWOT Analysis of key players (up to 3)

• Regional Segmentation

o Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

• Competitive Benchmarking

o Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

2.1 Abstract

2.2 Stake Holders

2.3 Research Scope

2.4 Research Methodology

2.4.1 Data Mining

2.4.2 Data Analysis

2.4.3 Data Validation

2.4.4 Research Approach

2.5 Research Sources

2.5.1 Primary Research Sources

2.5.2 Secondary Research Sources

2.5.3 Assumptions

3 Market Trend Analysis

3.1 Introduction

3.2 Drivers

3.3 Restraints

3.4 Opportunities

3.5 Threats

3.6 Application Analysis

3.7 End User Analysis

3.8 Emerging Markets

3.9 Impact of Covid-19

4 Porters Five Force Analysis

4.1 Bargaining power of suppliers

4.2 Bargaining power of buyers

4.3 Threat of substitutes

4.4 Threat of new entrants

4.5 Competitive rivalry

5 Global Flexible Plastic Packaging Coating Market, By Coating Type

5.1 Introduction

5.2 Epoxy Coatings

5.3 Acrylic Coatings

5.4 Urethane & Polyurethane Coatings

5.5 Lacquer Coatings

5.6 Plasma Coatings

5.7 Polyester Coatings

5.8 Phenolic Coatings

5.9 Water-Based Coatings

5.10 Solvent-Based Coatings

5.11 UV-Curable Coatings

5.12 Other Coating Types

6 Global Flexible Plastic Packaging Coating Market, By Material Type

6.1 Introduction

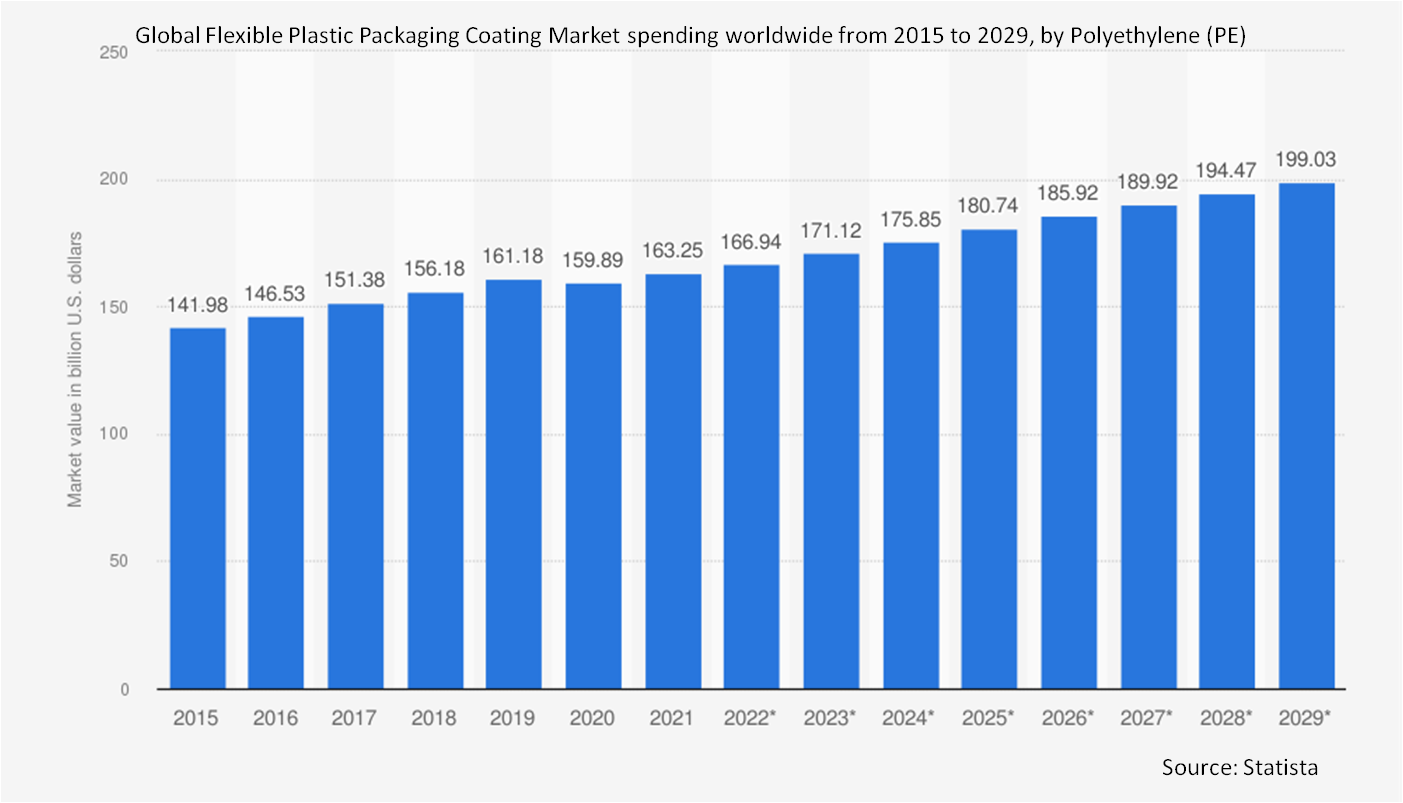

6.2 Polyethylene (PE)

6.2.1 Low-density Polyethylene (LDPE)

6.2.2 High-density Polyethylene (HDPE)

6.2.3 Linear Low-density Polyethylene (LLDPE)

6.3 Polypropylene

6.3.1 Biaxially-oriented Polypropylene (BOPP)

6.3.2 Cast Polypropylene (CPP)

6.4 Polyethylene Terephthalate (PET)

6.5 Polyamide (PA)

6.6 Polyvinyl Chloride (PVC)

6.7 Polyvinylidene Chloride (PVDC)

6.8 Ethylene Vinyl Alcohol (EVOH)

6.9 Polystyrene (PS)

6.10 Other Material Types

7 Global Flexible Plastic Packaging Coating Market, By Application

7.1 Introduction

7.2 Decorative

7.3 Protective

7.4 Heat Seal

7.5 Print Primer

7.6 Barrier Coatings

7.7 Other Applications

8 Global Flexible Plastic Packaging Coating Market, By End User

8.1 Introduction

8.2 Food & Beverage Packaging

8.3 Pharmaceutical Packaging

8.4 Cosmetics & Personal Care Packaging

8.5 Chemical Packaging

8.6 Consumer Durables/Electronic Goods Packaging

8.7 Automotive & Allied Packaging

8.8 Other End Users

9 Global Flexible Plastic Packaging Coating Market, By Geography

9.1 Introduction

9.2 North America

9.2.1 US

9.2.2 Canada

9.2.3 Mexico

9.3 Europe

9.3.1 Germany

9.3.2 UK

9.3.3 Italy

9.3.4 France

9.3.5 Spain

9.3.6 Rest of Europe

9.4 Asia Pacific

9.4.1 Japan

9.4.2 China

9.4.3 India

9.4.4 Australia

9.4.5 New Zealand

9.4.6 South Korea

9.4.7 Rest of Asia Pacific

9.5 South America

9.5.1 Argentina

9.5.2 Brazil

9.5.3 Chile

9.5.4 Rest of South America

9.6 Middle East & Africa

9.6.1 Saudi Arabia

9.6.2 UAE

9.6.3 Qatar

9.6.4 South Africa

9.6.5 Rest of Middle East & Africa

10 Key Developments

10.1 Agreements, Partnerships, Collaborations and Joint Ventures

10.2 Acquisitions & Mergers

10.3 New Product Launch

10.4 Expansions

10.5 Other Key Strategies

11 Company Profiling

11.1 BASF SE

11.2 Kansai Paint Co., Ltd.

11.3 Akzo Nobel N.V.

11.4 Koninklijke DSM N.V.

11.5 Bostik SA

11.6 Michelman, Inc.

11.7 Jamestown Coating Technologies Company

11.8 Paramelt B.V.

11.9 American Packaging Corporation

11.10 Sierra Coating Technologies LLC

11.11 Allnex Group

11.12 PPG Industries, Inc.

11.13 Schmid Rhyner AG

11.14 Wacker Chemie AG

11.15 Plasmatreat GmbH

List of Tables

1 Global Flexible Plastic Packaging Coating Market Outlook, By Region (2024-2032) ($MN)

2 Global Flexible Plastic Packaging Coating Market Outlook, By Coating Type (2024-2032) ($MN)

3 Global Flexible Plastic Packaging Coating Market Outlook, By Epoxy Coatings (2024-2032) ($MN)

4 Global Flexible Plastic Packaging Coating Market Outlook, By Acrylic Coatings (2024-2032) ($MN)

5 Global Flexible Plastic Packaging Coating Market Outlook, By Urethane & Polyurethane Coatings (2024-2032) ($MN)

6 Global Flexible Plastic Packaging Coating Market Outlook, By Lacquer Coatings (2024-2032) ($MN)

7 Global Flexible Plastic Packaging Coating Market Outlook, By Plasma Coatings (2024-2032) ($MN)

8 Global Flexible Plastic Packaging Coating Market Outlook, By Polyester Coatings (2024-2032) ($MN)

9 Global Flexible Plastic Packaging Coating Market Outlook, By Phenolic Coatings (2024-2032) ($MN)

10 Global Flexible Plastic Packaging Coating Market Outlook, By Water-Based Coatings (2024-2032) ($MN)

11 Global Flexible Plastic Packaging Coating Market Outlook, By Solvent-Based Coatings (2024-2032) ($MN)

12 Global Flexible Plastic Packaging Coating Market Outlook, By UV-Curable Coatings (2024-2032) ($MN)

13 Global Flexible Plastic Packaging Coating Market Outlook, By Other Coating Types (2024-2032) ($MN)

14 Global Flexible Plastic Packaging Coating Market Outlook, By Material Type (2024-2032) ($MN)

15 Global Flexible Plastic Packaging Coating Market Outlook, By Polyethylene (PE) (2024-2032) ($MN)

16 Global Flexible Plastic Packaging Coating Market Outlook, By Low-density Polyethylene (LDPE) (2024-2032) ($MN)

17 Global Flexible Plastic Packaging Coating Market Outlook, By High-density Polyethylene (HDPE) (2024-2032) ($MN)

18 Global Flexible Plastic Packaging Coating Market Outlook, By Linear Low-density Polyethylene (LLDPE) (2024-2032) ($MN)

19 Global Flexible Plastic Packaging Coating Market Outlook, By Polypropylene (2024-2032) ($MN)

20 Global Flexible Plastic Packaging Coating Market Outlook, By Biaxially-oriented Polypropylene (BOPP) (2024-2032) ($MN)

21 Global Flexible Plastic Packaging Coating Market Outlook, By Cast Polypropylene (CPP) (2024-2032) ($MN)

22 Global Flexible Plastic Packaging Coating Market Outlook, By Polyethylene Terephthalate (PET) (2024-2032) ($MN)

23 Global Flexible Plastic Packaging Coating Market Outlook, By Polyamide (PA) (2024-2032) ($MN)

24 Global Flexible Plastic Packaging Coating Market Outlook, By Polyvinyl Chloride (PVC) (2024-2032) ($MN)

25 Global Flexible Plastic Packaging Coating Market Outlook, By Polyvinylidene Chloride (PVDC) (2024-2032) ($MN)

26 Global Flexible Plastic Packaging Coating Market Outlook, By Ethylene Vinyl Alcohol (EVOH) (2024-2032) ($MN)

27 Global Flexible Plastic Packaging Coating Market Outlook, By Polystyrene (PS) (2024-2032) ($MN)

28 Global Flexible Plastic Packaging Coating Market Outlook, By Other Material Types (2024-2032) ($MN)

29 Global Flexible Plastic Packaging Coating Market Outlook, By Application (2024-2032) ($MN)

30 Global Flexible Plastic Packaging Coating Market Outlook, By Decorative (2024-2032) ($MN)

31 Global Flexible Plastic Packaging Coating Market Outlook, By Protective (2024-2032) ($MN)

32 Global Flexible Plastic Packaging Coating Market Outlook, By Heat Seal (2024-2032) ($MN)

33 Global Flexible Plastic Packaging Coating Market Outlook, By Print Primer (2024-2032) ($MN)

34 Global Flexible Plastic Packaging Coating Market Outlook, By Barrier Coatings (2024-2032) ($MN)

35 Global Flexible Plastic Packaging Coating Market Outlook, By Other Applications (2024-2032) ($MN)

36 Global Flexible Plastic Packaging Coating Market Outlook, By End User (2024-2032) ($MN)

37 Global Flexible Plastic Packaging Coating Market Outlook, By Food & Beverage Packaging (2024-2032) ($MN)

38 Global Flexible Plastic Packaging Coating Market Outlook, By Pharmaceutical Packaging (2024-2032) ($MN)

39 Global Flexible Plastic Packaging Coating Market Outlook, By Cosmetics & Personal Care Packaging (2024-2032) ($MN)

40 Global Flexible Plastic Packaging Coating Market Outlook, By Chemical Packaging (2024-2032) ($MN)

41 Global Flexible Plastic Packaging Coating Market Outlook, By Consumer Durables/Electronic Goods Packaging (2024-2032) ($MN)

42 Global Flexible Plastic Packaging Coating Market Outlook, By Automotive & Allied Packaging (2024-2032) ($MN)

43 Global Flexible Plastic Packaging Coating Market Outlook, By Other End Users (2024-2032) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

List of Figures

RESEARCH METHODOLOGY

We at ‘Stratistics’ opt for an extensive research approach which involves data mining, data validation, and data analysis. The various research sources include in-house repository, secondary research, competitor’s sources, social media research, client internal data, and primary research.

Our team of analysts prefers the most reliable and authenticated data sources in order to perform the comprehensive literature search. With access to most of the authenticated data bases our team highly considers the best mix of information through various sources to obtain extensive and accurate analysis.

Each report takes an average time of a month and a team of 4 industry analysts. The time may vary depending on the scope and data availability of the desired market report. The various parameters used in the market assessment are standardized in order to enhance the data accuracy.

Data Mining

The data is collected from several authenticated, reliable, paid and unpaid sources and is filtered depending on the scope & objective of the research. Our reports repository acts as an added advantage in this procedure. Data gathering from the raw material suppliers, distributors and the manufacturers is performed on a regular basis, this helps in the comprehensive understanding of the products value chain. Apart from the above mentioned sources the data is also collected from the industry consultants to ensure the objective of the study is in the right direction.

Market trends such as technological advancements, regulatory affairs, market dynamics (Drivers, Restraints, Opportunities and Challenges) are obtained from scientific journals, market related national & international associations and organizations.

Data Analysis

From the data that is collected depending on the scope & objective of the research the data is subjected for the analysis. The critical steps that we follow for the data analysis include:

- Product Lifecycle Analysis

- Competitor analysis

- Risk analysis

- Porters Analysis

- PESTEL Analysis

- SWOT Analysis

The data engineering is performed by the core industry experts considering both the Marketing Mix Modeling and the Demand Forecasting. The marketing mix modeling makes use of multiple-regression techniques to predict the optimal mix of marketing variables. Regression factor is based on a number of variables and how they relate to an outcome such as sales or profits.

Data Validation

The data validation is performed by the exhaustive primary research from the expert interviews. This includes telephonic interviews, focus groups, face to face interviews, and questionnaires to validate our research from all aspects. The industry experts we approach come from the leading firms, involved in the supply chain ranging from the suppliers, distributors to the manufacturers and consumers so as to ensure an unbiased analysis.

We are in touch with more than 15,000 industry experts with the right mix of consultants, CEO's, presidents, vice presidents, managers, experts from both supply side and demand side, executives and so on.

The data validation involves the primary research from the industry experts belonging to:

- Leading Companies

- Suppliers & Distributors

- Manufacturers

- Consumers

- Industry/Strategic Consultants

Apart from the data validation the primary research also helps in performing the fill gap research, i.e. providing solutions for the unmet needs of the research which helps in enhancing the reports quality.

For more details about research methodology, kindly write to us at info@strategymrc.com

Frequently Asked Questions

In case of any queries regarding this report, you can contact the customer service by filing the “Inquiry Before Buy” form available on the right hand side. You may also contact us through email: info@strategymrc.com or phone: +1-301-202-5929

Yes, the samples are available for all the published reports. You can request them by filling the “Request Sample” option available in this page.

Yes, you can request a sample with your specific requirements. All the customized samples will be provided as per the requirement with the real data masked.

All our reports are available in Digital PDF format. In case if you require them in any other formats, such as PPT, Excel etc you can submit a request through “Inquiry Before Buy” form available on the right hand side. You may also contact us through email: info@strategymrc.com or phone: +1-301-202-5929

We offer a free 15% customization with every purchase. This requirement can be fulfilled for both pre and post sale. You may send your customization requirements through email at info@strategymrc.com or call us on +1-301-202-5929.

We have 3 different licensing options available in electronic format.

- Single User Licence: Allows one person, typically the buyer, to have access to the ordered product. The ordered product cannot be distributed to anyone else.

- 2-5 User Licence: Allows the ordered product to be shared among a maximum of 5 people within your organisation.

- Corporate License: Allows the product to be shared among all employees of your organisation regardless of their geographical location.

All our reports are typically be emailed to you as an attachment.

To order any available report you need to register on our website. The payment can be made either through CCAvenue or PayPal payments gateways which accept all international cards.

We extend our support to 6 months post sale. A post sale customization is also provided to cover your unmet needs in the report.

Request Customization

We offer complimentary customization of up to 15% with every purchase. To share your customization requirements, feel free to email us at info@strategymrc.com or call us on +1-301-202-5929. .

Please Note: Customization within the 15% threshold is entirely free of charge. If your request exceeds this limit, we will conduct a feasibility assessment. Following that, a detailed quote and timeline will be provided.

WHY CHOOSE US ?

Assured Quality

Best in class reports with high standard of research integrity

24X7 Research Support

Continuous support to ensure the best customer experience.

Free Customization

Adding more values to your product of interest.

Safe & Secure Access

Providing a secured environment for all online transactions.

Trusted by 600+ Brands

Serving the most reputed brands across the world.